6

The Advice

22 October, 2021

This text is interactive and best experienced on a desktop. As you scroll, click and hover over underlined sections to reveal extra images, animations and sounds.

• • •

Sit down, please.

My apologies for the state of the place. I’m still waiting on the wall-chippers to finish with the wall-refurb. They’ve been chipping off paint for the last two weeks. You know what it’s like. A “couple of days’ work” becomes “a couple of weeks sitting around chipping paint from the walls while I’m trying to review loan agreements and advise accordingly.” Then they start telling me, “ohhh you need a painting for this wall. And I say, no I don’t, actually, I like the wall bare. I like the sheer pastel face of it. Just my face staring at the wall’s face and that’s how I like it. What do you wall-chippers know about paintings anyway?”

But then they show me these paintings on their phones and as they’re scrolling through these images I’m starting to think, you know what? I actually like these paintings! And the next thing I know they’re hauling this thing from Christie’s up the stairs and straight onto my wall and now I’m staring at this painting all day long.

It’s a Van der Helst knockoff, sure. The paint-chippers made no secret of that. Painted by a fellow who lives in Dandenong, they say. “Banquet of the Amsterdam Civic Guard in Celebration of the Peace of Münster”, they call it. Isn’t that right, wall-chippers? Yep. I thought so.

Anyway. I should begin the advice.

Sit down. Please. If you can find a seat! Sorry, just move that pile of—yep, that can go into this…here…folder. Great. Thanks.

So! Here we are. The Contract. The Debt. The Obligations. My Ensuing Advice.

Now. Just so you’re aware up front: I’ll be charging a fixed fee for this advice. I won’t be charging in six-minute increments, which is the practice of some of my less principled ‘associates’ who talk your ear off, all the while charging sixty dollars per six-minute interval.

My fixed-fee practice means it’s $2,700 plus GST for the contract review and advice in this particular area of law in which I profess to be competent. I mean, that’s the scope of our retainer, which of course defines the limits, the edges, the borders, the scope of our relationship. Think of it as an invisible fence, capturing all the things we’re going to do together—reviewing the contract, emailing, talking on the phone, talking in person—all confidential of course, our conversations safely muted by the Gatekeepers of Legal Professional Privilege who watch over our private sanctuary. And because you’ve retained me that means I’m not going anywhere. I’m yours while retained. I will reside in our secret retainer-space bound as I am by the Solicitor’s Ethical Code of Conduct.

We’re in here:

Solicitor and Client

Good? Good. I note that nowhere within the above fence-line do we see wall-chippers (meaning that now is a good time for the wall-chippers to exit the room while I expound my advice). Thank you, wall-chippers. You can leave your chippers at the door. Thank you. Thanks.

Okay. Now, let’s take a look at this thing. And begin the advice. Alright. Let me see. What. Do. We. Have. Here.

The Borrower [that’s you] will comply with the relevant timeframe for the Loan Facility as specified by the Lender.

Yep. Here come the definitions:

Loan Facility means a credit arrangement whereby the Borrower borrows money in an agreed amount from the Lender.

Hmmm.

Clause 8 (a) (ii) in an event of default the Lender is entitled without further notice to—

Okay. This is my advice.

You must first understand your orientation within the legal landscape.

As we are dealing with a Loan Agreement, we are currently in The Lands of Contract. I can competently guide you through these lands. I walk here regularly and tend to the various gardens scattered from place to place. I should say, specifically, we are in the Meadows of Contract Formation and, even more specifically, the Gardens of Terms and Conditions. You may inspect at your leisure the floral decorations of a typical Default Clause or the long, tendril-like necks of the Guarantee Terms.

Over yonder, you will find a strip of Conditional Carnations.

I refer you to them simply because they contain the normal and expected “conditions precedent” one might find in a contract like yours, a loan agreement. I, of course, did not plant these flowers. I merely tend to them and ensure their ongoing survival along with many other solicitors, or “Officers of the Court”, as we sometimes refer to ourselves. Should you choose to peruse the Conditional Carnations, you may encounter these Officers, watering cans in hand (they will likely attempt to seduce you to enter into new retainers with them or with their firms, but I assure you, as I have already stressed, my competency in this area and my quite reasonable fees [all things considered] should persuade you to remain within the boundaries of our existing retainer, where, I hope, you still feel most comfortable).

Come. Let’s view the Conditional Carnations. Join me. Here. See! There we go. A beautiful one:

10.3 Notwithstanding anything herein or otherwise implied, the Lender is not obliged to grant any facility to the Borrower pursuant to this Agreement unless and until:(a) the Borrower provides a Notice of Information to the Lender in writing, specifying the purpose or purposes for which the facility is requested.

Long story short, this beautifully crafted carnation has been pruned and watered for hundreds of years, prior to its inclusion in its present form in your loan agreement. While its outward appearance may have changed over time with the different weathers and Officers who have tended to it, in one form or another, it has been planted in loan agreements all the way back to a date somewhere around 1580, when it emerged originally in the context of Estates and the feudal system of land tenure (of course, in the 18th century the modern dichotomy between The Condition and The Warranty began to emerge and evolve but that’s a story for another day).

Now. If you listen carefully as you explore these gardens, you may hear the pleasant sounds of the local fauna. These lands are populated by a rich biosphere packed with all sorts of creatures. Listen. There is the sound of a Long-beaked Facility-Drawdown Dove, which delicately sings out your obligations with respect to withdrawals from the loan facility. There it is again.

And that! Hear that? That’s the famous sound of the Event of Default Noddy, screeching out to mark the consequences of your failures to repay the loan, thereby signalling the intervention of the law into your private life and the possible restraint of your assets.

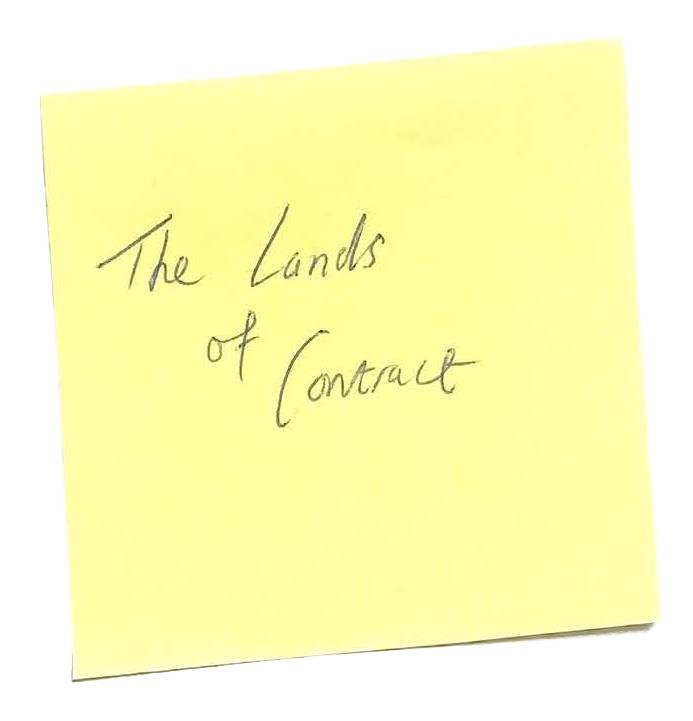

Post it note?

This type of law—contract law—can be contrasted with other forms of law, like the law of Tort (which derives from the Latin word, tortus, meaning “wrong”). Wrong. “Tort” law generally tries to allocate responsibility for different types of losses. It consists of obligations that are imposed upon you (and on me, and on all of us) whether or not we agree. For instance, we all owe a duty of care to each other when we drive our automobiles. If I drive my automobile negligently and crash my automobile into your automobile, I may breach the duty of care I owe to you and commit a tort. Torty Tort.

While contract and tort share similar historic roots (which is surely what Deane J was referring to in Hawkins v Clayton (1988) 164 CLR 539; 62 ALJR 240 at 584 when he said that “[t]he law of contract and the law of tort are, in a modern context, properly to be seen as but two of a number of imprecise divisions, for the purpose of classification, of a general body of rules constituting one coherent system of law”) they are today generally considered distinct.

In any case, to stray further into the vast Tortious Territories today would be to step far beyond the walls of my retainer, which I do not intend to do.

Note! This is the point at which, were I one of my less principled colleagues, I would be marking the end of the first six-minute block of time and the commencement of the second, meaning that this advice would have cost you $60 up to and including this point. But as afore mentioned, that is not my practice. My retainer is not restrained by temporal boundaries. However, just so you’re fully aware of the costs savings of my billing practice, and to remind you of how my less principled colleagues regularly charge, I will draw a line under each six-minute parcel of advice.

Should you walk North, South, East or West from this point, you will encounter all the hallmarks of a contract in one floral form or another. Eventually, you will hit what will appear to be an artificial wall, a bit like this:

Nothing special about it. Just a gypsum plasterboard white wall in the middle of this legal landscape. It is the boundary of this place, the edge of these gardens in which we presently frolic. Pass this wall and you will enter new lands, of which I assure you there are many, stretching in every direction as far as you can possibly imagine.

It is my strong and urgent and, I hope, clear advice that you attempt, at all costs, to remain within the surrounding walls of Contract Formation and stray not into the soggy marshlands commonly known as Contractual Disputes. I will do my best to guide you fairly and competently away from such swamplands through the diligent and meticulous performance of my retainer. But one can never be certain and so, for the record (and rest assured this will be confirmed in writing via email correspondence shortly after this meeting), I unambiguously advise you to avoid at all costs the marshlands. They are populated by unequitable sinkholes, repudiatory pits and the oft-unforgiving sludge of the Common Law. And, what’s more, you risk encountering one of the esteemed Magistrates who dwell in this region. They wade through the marshes, bubbling and groaning as they heave their tired bodies through the slop.

You may simply be sludging along, minding your own business, when you encounter what appears to be a mere ‘bubbling’ amongst the wet-dirt. Before you know it, a robed assailant is upon you, crying out: “You there! I am a Proper Officer of this Rightful Place, authorised by Order 61 of the Magistrates Court General Civil Procedure Rules 2020 to hear any Summons for Examination made under section 14 or 17 (and made in Form 61F) of the Judgment Debt Recovery Act 1984, what business have you before this Place?” And should you fail to respond adequately (or at all), the Magistrate has the power by virtue of order 61.07 of the Rules to issue a Warrant of Apprehension, thereby formally bringing your person before a court of law.

Should you stray further, beyond the swamplands into the mountainous regions in the North, it may be the case that you encounter a Judge from one of the higher courts (i.e. the County, the Supreme, the Federal, the High Courts of these Lands). Should you come before such a Judge, I warn you: each of them has walked the legal, economic and regulatory lands for years. They have hiked contractual mountains and traversed promissory gullies with exclusion clauses a mile long. They will observe your body, scan your eyes, hear your voice, letting it pass (dribble or flow) through their judicial ears and there will be judgment of your person, of your intentions and of your behaviour pre, during and post the formation of this contract. Your rights and liabilities will be determined not by reference to your subjective beliefs or understandings, but by reference instead to your words or conduct, a judgment as to what those words or that conduct would lead a reasonable person in the position of the other party [in this case, the Lender] to believe. Inferences will be drawn.

because as the High Court said in Taylor v Johnson (1983) 151 CLR 442 at [428] per Mason ACJ, Murphy and Deane JJ, “the law is concerned not with the real intentions of the parties but with the outward manifestations of those intentions.”

I warn you: beware your outward manifestations should you take any further steps in these lands. Beware the scouts and sentinels of the Court that peruse this place. They will be watching. Beware the sweat on your forehead, the stench of your underarms. Beware your outward manifestations and how they may be perceived by others, by those roving eyes of the Court, those wandering ears. As is regularly professed by Judges and Magistrates alike—the Court’s ears do roam. You may find a judicial ear nestled in the leaves of the local Agatha Tree. Listening. You may find an eye in your cereal bowl, swimming in your milk, or buried in your packet of crisps—discover the iris as your fingers rustle through the chips and seasoning. Beware—the law listens to your murmurs. Each movement may be scrutinised by the eyes and ears of the Court, those wandering bits and pieces. Beware.

In any case! Here we are, located clearly and firmly in Pre-Contract. Should you agree to the terms of this contract, it will become a legally enforceable agreement, meaning that if you (the Borrower) or your counterpart (the Lender) break the promise(s) contained therein, you submit to the binding decision of a Court of Law to force you to honour your promise(s).

Traditionally, contracts are classed as a form of “private law”: two or more “private” individuals freely agreeing to be bound by their promises. This view of contract law developed in England in the 19th century and so it is of course influenced by the values of that time. The law thinks of us all as self-governing, bounded bodies with the capacity to make rational decisions. The law does not think of us as an assemblage of anaerobic bacteria (there are around 600 different species in our mouths) and macrophages and other microbes that jostle and gyrate in symbiosis with our changing environments and the various non-human entities we encounter, be they Carnations or Cardamoms or oak trees or streams or birds of prey, our bodily walls tramped upon by our immediate neighbours as we engulf and are engulfed by them ad infinitum. No. The law does not see us this way. Despite the very public nature of our bodies, the law views each and every one of us as a “private” individual, freely contracting with one another as per this very loan agreement, the subject of my advice.

Here:

The Lender grants to the Borrower a loan facility of an amount not exceeding the specified amount.

That’s a promise. Right there. You can see it written down on paper but you’ve instructed me that this whole “loan agreement” started with a conversation between you and the Lender, am I right? I am? Okay. That’s what I thought. Promises often first emerge from the mouth and are then assisted by the hand(s) when they are recorded as written agreements. The law recognises both types of agreements (oral and written) as potentially enforceable.

So. You and the Lender are chatting away. You’re having a conversation about a topic of your mutual interest and/or convenience. And then the Lender offers you the loan, verbally. You accept, verbally. Two private persons engaging in an exchange of sounds and noises that emerge from your mouths. These sounds start somewhere inside your bodies. That’s where they’re cooked up. In the stomach or the gullet or the upper chest region. The body warms the promise. The body wraps around the sounds until they are ready to emerge and then they vibrate in your throat-departments before rolling over your tongues:

“How about a loan? Okay, I accept your loan. Should we sign a loan agreement?”

Let it roll over your tongue. “Loan Agreement.” Feel it push past your teeth. Say it with me:

“Loan Agreement.”

That’s good! Good. That’s very good.

Let’s feel some more of the terms in your mouth:

“The Lender is not obliged, either now or in the future, to provide further facility to the Borrower”

Good.

Promises, right? Promises that find their way out the hole in your face and enter the world. Then they slip into each other’s ears:

We’re always entering contracts and making promises. All the time. You enter a contract when you buy a chocolate milk, or a delicious package of Thins Crisps from the local Super-Mart. You also enter a contract when you agree to supply thirty-two tonnes of aluminium to a distribution centre near Kangaroo Island, but that’s delving into confidential information about one of my clients so I will delve no further.

Whenever sounds enter the world and become words, and if those words legally constitute a “promise”, then the law will respect the power of that promise to bind the body of the promisor by entitling the promisee to enforce the promise in a Court of Law. The words of the promisee become a bridge between two bodies, tying them together and dictating their private lives.

In your case, and I don’t mean to scare you, but your promises are a pair of word-handcuffs, ensuring that you honour your obligation to repay the loan:

So, by way of summary: your promise is first hugged and nurtured inside your body, then when it leaves your mouth it betrays you, reverting back to bind your wrists. Which reminds me—the wrists are important because they connect the hands to the rest of the body. And the activities of the hands can be very important in The Lands of Contract. A handshake, for instance, is an important gesture in sealing promissory deals, such as peace negotiations, as was the case in my knockoff Van der Helst, where in the headquarters of the Crossbowmen’s Civic guard in Amsterdam in 1648, Captain Cornelis Jansz Witsen shook the hand of Johan Oetgens van Waveren, celebrating an end to the Eighty Years War and the Seven United Provinces of the Netherlands’ independence from the Spanish Empire. The Peace of Münster, they call it.

Look at those hands!

All those cross bowed bodies still lying out on the battlefield, those sworded-arms and ruffled noses, those grunts and groans and poorly-formed words,

then all that negotiating and swearing of oaths. All those promises and representations, all that trumpeting. The verbal and bodily posturing is all bound up in the hands of Witsen and Waveren, as are the ramifications of peace after years of war. Their hands bind them, a bridge between their bubbling, groaning assemblages of microbes. Each of them crosses the bounded bodily threshold into the landscape of mutual obligations. The shaking of those little Dutch hands brought forth a new era of mercantile contracts between private individuals in different parts of Europe, parts that were, for eighty years, divided by war—

(please note: my commentary on the Peace of Münster [and on any “treaty” for that matter] and any further commentary by me about the Laws of War or Nation-State Arbitrations or International Law is not to be taken as legal advice and is provided simply by way of academic observation. For me to posture or proclaim professional competency in those areas, in those foreign territories, would be to stray beyond the walls of my comfort [and beyond the boundaries of our retainer], which is something I am not willing to do. No reliance should be placed by you on my commentary supra and any liability by me for any such comments is strictly limited).

Anyway.

We should, after all, look a little closer at some of the key terms of the contract. Shall we? We shall. Okay.

Where are we…

Clause 16 (a) roman numeral one:

Interest shall be calculated and payable on the outstanding amount on the dates outlined in Annexure 3 to this Agreement.

Okay. Yes.

Roman numeral two:

The Borrower will repay interest at the amount agreed unless, at the discretion of the Lender, it is determined that the Borrower repay interest at a different rate, including at a higher rate should the Lender so decide.

Hmm. Bit concerning. Don’t really want your wrists tied up when you’re facing that term. Hm. Letting the Lender decide how much interest you pay. All written out carefully in Times New Roman. They just had to use that most brutal of fonts to express that most brutal of terms, didn’t they? Hm. Using that tasty flourishing font with its little embellishments and flicks on its tails and feet. Combining all that in a debt contract! A loan agreement! Strict Roman Hands for a Strict Roman Font. Sturdy hands. Now they’re using them on your skin. You, the debtor—they’re holding you rough in this term, you know that? They’re holding you really rough. They’re gripping you. Strong. They’ll pull you through the other clauses like this, drag you through the other terms. They don’t care if your body’s all scratched up from the thorned provisions. Hm.

Clause 16 (b)

The Borrower is to pay to the Lender on demand any amount outstanding pursuant to this Agreement.

Typical. Hm.

Clause 17 (a)

The Loan Facility shall be secured by the Securities, consisting of mortgages and deeds.

You could kick up a fuss about this one. But it may not be worth your time.

Clause 17 (b)

Time shall be of the essence of this Agreement.

Typical.

Clause 18 (a)

The Guarantors jointly and severally unconditionally guarantee to the Lender the payment of the Principal, interest, damages and other moneys payable by the Borrower pursuant to this Agreement.

Quite ordinary.

Clause 18 (b)(i)

Hm.

Now. The quite large hole in this particular clause is troubling. Yes. Concerning. Advising about holes, such as this one, is usually beyond the scope of my retainer. In fact, nothing in my retainer requires me to advise on physical alterations to the Loan Agreement itself, including, but not limited to, holes penetrating the surface. Any liability I may incur for such advice is strictly limited. Yet, despite my misgivings, I am prepared to offer you some general guidance with respect to this hole. Hm. Yes. I should note that any contractual term contained within the hole appears to be unreadable and potentially unenforceable. It is trite law to state that obligations buried inside a hole cannot bind a party to an agreement.

I do draw your attention to Darrington J’s helpful commentary on this issue in Sleeper Pty Ltd v Molton (1943) ER 431 at [23] where it was stated that “[o]bligations existing inside a hole or any penetrated surface bear a certain resemblance to obligations that incubate inside the body before emerging from the mouth hole. Such obligations, invisible prior to their emergence, are not binding upon another person until they enter the world. It follows that any obligations buried within a hole are likely to be unenforceable at law.”

This hole does appear to be particularly gaping in nature. Dark interior. Significant depth (perhaps leading into foreign lands, beyond these familiar Meadows of Contract Formation, perhaps leading further, even, than the Gardens of Terms and Conditions). Hm. I fear the worst. Yes. I fear that ears may be lurking within this hole or, perhaps, eyes, or even noses may have found their way into this very room, entering through this here hole. Hm. These body parts may even belong to the Lenders. We should stop this advice immediately. Our confidentiality has been compromised.

Our fence has been breached. This hole may in fact indicate that we are now in the realm of a Contractual Dispute.

Tread carefully. Please. Hold your tongue and I will hold mine.

I hereby conclude this advice.

Wall-chippers? Wall-chippers! Yes. You may re-enter, we have concluded the legal advice. Welcome back. Please continue chipping. Thank you. And please ensure you do not chip your way through the entirety of the plasterboard. I fear what outside ears may be attempting to hear my private, confidential, and legally privileged conversations herein.

Well! Now that we have traversed the terrain of this Loan Agreement, we may return to talking about matters peripheral to the legal advice. Firstly, as previously discussed, the cost of this advice today is $2,700 plus GST and I do require payment within seven days of the provision of the advice by electronic transfer to my previously provided banking account. Your swift payment would be appreciated.

Finally, before you take your leave of my office, allow me to relay to you one final piece of advice (of course, anything I am about to say is advice of a general nature and should not be construed as legal advice). As you leave this office, as you set out into the world and potentially sign this here Loan Agreement (thereby accepting its binding obligations), before you enter more contracts, purchasing a chocolate milk from the local cafeteria, for instance, before you grapple with any further obligations—be aware of your body. Think of how you move through this world, because—and I’m sure the wall-chippers can agree with this—each step matters. Every action or inaction you take triggers legal consequence, whether or not that consequence is subsequently enforced by another party. You are but a cog in this ever grinding, ever working, largely invisible legal machine. As am I. As are these here wall-chippers. Each handshake. Each nod of the chin. Flick of the eyes. Groan of the mouth. It’s all a fleshy, frothing, churning marinade. And like the microbiomes beneath our skin, we are all in here together. Swimming.